What you are owed for your Homeowners Insurance claim is a complicated question. The short answer is you are owed Replacement Cost Value. However, in Florida there are two different theories of recovery regarding how a Homeowners claim should be paid and Florida law incorporates both theories into your recovery. Naturally, things can get a bit confusing. The first theory is called Actual Cash Value otherwise known as ACV. ACV is defined as the Replacement Cost Value minus deprecation or in other words Fair Market Value.1 Fair Market Value accounts for the property’s depreciated condition.2 The second theory is known as Replacement Cost Value otherwise known as RCV. Replacement Cost Value is exactly what it sounds like it’s the cost to repair or replace your property, or otherwise restore it to its pre-loss condition.

Fla. Stat. § 627.7011(1)(a) states that prior to issuing a homeowners insurance policy an insurer must offer a policy or endorsement providing that any loss that is repaired or replaced will be adjusted on the basis of replacement cost to the dwelling not exceeding policy limits, i.e. by law, your insurance carrier must initially offer you an RCV policy. Failure of the carrier to get a signed written refusal of RCV coverage creates a presumption that it was not offered.3

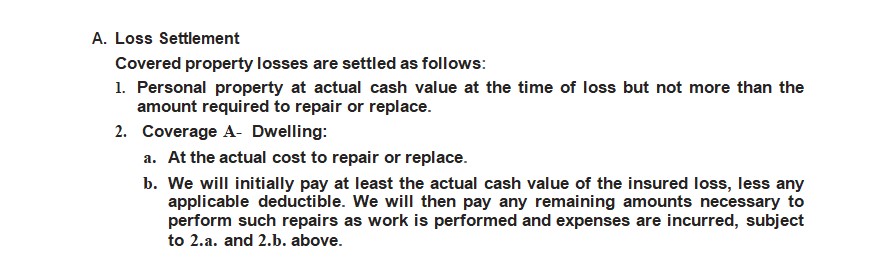

Now this is where it gets confusing. Fla. Stat. § 627.7011(3)(a) also states that upon acceptance of a claim, the insurer must initially pay ACV minus any applicable deductible and pay any remaining amounts necessary to perform such repairs as work is performed and expenses are incurred. As a result many Homeowners’ Insurance policies Loss Settlement Provisions read something like this:

What does this mean? This means that at upon acceptance of your claim, the insurance carrier only has an obligation to pay ACV amount (the lesser of the two), despite the fact that you purchased an RCV policy. What’s worse, is that often times your insurance carrier under adjusts the ACV payment and implies that the ACV payment is the total amount you will receive for your claim. This is why it is important to speak to an Attorney who knows the value of your claim and knows what you should be compensated. As the Third District Court of Appeal stated in Vazquez v. Citizens Property Insurance Corp., 304 So.3d 1242 (Fla. 3rd DCA 2017) “The payment of an amount by an Insurance Carrier which it claims to be satisfaction of the value of the loss does not create a legal presumption that the amount paid is the Actual Cash Value of the covered loss”.

{kind=link}

{kind=link}

{kind=link}